Supply refers to the various amounts of a good which the sellers are willing and able to sell at any given price per unit of time.

Factors Influencing Supply (Determinants of Supply)

1. Price of that commodity :

Higher the price, more will be the quantity supplied.

2. Price of other commodities :

The relative profitability of other commodities affects the relative attractiveness to firms for different line of production. Firms undertake to supply new commodity with high profitability.

3. Goals of the producers:

Firms may select more commodities for supply, based on their goal to expand the market, serve the interest of the society etc. For this study we, however, consider profit maximization as the single important goal of the firms.

4. State of Technology:

The improvement in the technique of production

essentially leads to increase in supply. Inventions

and innovations make it possible to produce more

and/or better commodities.

5. Cost of production:

If the cost of production factors increases the

producer decides to produce less and supply of that

commodity is restricted and vice versa. Here it is

assumed that other things being equal.

6. Availability of raw materials & other inputs:

Supply is adversely affected in absence of free and

regular availability of required amounts of raw

materials and other inputs.

7. Climate and forces of nature:

Especially in the sphere of agriculture, climate

plays a major role in supply. Both timing & quantum

of rains have direct effect on supply of food

grains, fruits and other farm or animal products.

8. Time element:

In a short period, supply cannot be changed to

match change in demand or price. With change in

prices or demand supply gets adjusted after a

certain period that is required to readjust inputs,

capacity or process of production.

9 Transport Facilities:

Availability of transport facilities enhances

supply and enlarges the markets for a commodity.

10 Taxation and subsidy:

The tax policy of the Government influences

‘production initiative’ of entrepreneurs and prices

for commodities. Both have direct effect on supply.

11 Expectations regarding future prices:

These lead to either speculative hoarding ( less

supply) or even distress sales. ( more supply).

The Supply Function :

As the quantity supplied of commodity X is a

function of about eleven variables listed above,

the function can be written as

Qxs =f(Px,p,c,G,T,....etc)

Where,

Px is price of X

P is price of commodities other than X

c is cost of production.

G is goals of he producers etc.

assume that all the other variables are held

constant and establish relation between Price of X

and Quantity supplied of X.

Or

Qxs =f(Px)

where,

P1 =P0; c=c0; G=G0;etc.

The Law of Supply :

As stated above the law of demand assumes factors

other than price of commodity remain constant.

The law states “other things remaining the same the

quantity supplied of a commodity X is directly

related to its price.”

The Supply Curve :

Supply schedule indicates different quantities of

commodity X supplied at various prices. When these

are plotted on a graph we get a supply curve as

below. This curve slopes upwards from left to right

{kind=link}

{kind=link}

It is customary to represent price on Y axis and

quantity on the X axis.

What are other things that must remain the same ?

Other things that must remain the same are :-

- Cost of production.

- Methods of production.

- Availability of inputs.

- Transport facilities.

- Weather conditions.

- Tax structure.

- Goals of producers.

- Sellers’ expectations about future prices.

-

Prices of other goods.

Backward Bending Supply Curve of labour :-

An interesting exception to the law of supply is

provided by the supply curve of labour. Here we

come across a peculiar phenomenon. As wages

increase, labour supply in the form of hours worked

per day goes up; but only up to a certain point,

say 12 hours. After reaching that point worker,

finds that same wages could be earned, by working

lesser hours at the increased rate. Thereafter the

supply reduces. This is called backward bending

supply curve of labour and is an exception to the

law of demand.

Reservation Price and Supply :

The reservation price of a seller is that price

below which the seller would not sell the

commodity. The seller wants to guard his profit

margin.

The reservation price of a seller depends on –

► The sellers need for liquid cash.

If the seller wants cash urgently, his reservation

price would be low as he needs to convert the goods

into cash urgently.

► The durability of commodity.

If the commodity is perishable, the reservation

price would be low as seller needs to convert goods

into cash in a short time.

► The expectations about future price.

If the seller expects that the prices would rise in

future, he would increase his reservation price and

vice versa.

► The cost of storage.

High cost of storage would make seller to dispose

off his stocks early, thereby bringing down the

reservation price.

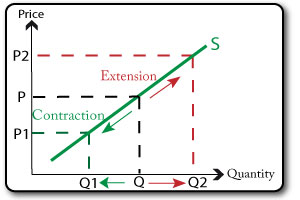

Variations and changes in Supply :

(Movements along the curve vs. shifts of curves)

If we consider changes in price of a commodity as

the only factor influencing its quantity supplied,

then we experience movements on the same curve. We

either have extension or contraction of supply.

Movement along the Supply Curve (Price)

A change in price causes a movement along the curve The higher the price of a product, the more suppliers will produce.. If the price rises then supply will rise, this is known as an extension in supply. The lower the pice of a product the less will be supplied. If the price falls then supply will fall, this is known as an contraction in supply.

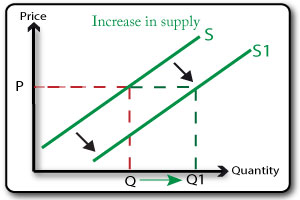

On the other hand when factors other than price of

the commodity influence supply for that commodity,

then we have either increase or decrease in supply

shown by complete shifts in the supply curve.

Shift of the Supply Curve

A shift of the supply curve represents an increase or decrease in the quantitiy supplied at each & every price. Causes of shifts in supply:

A shift of the supply curve represents an increase or decrease in the quantitiy supplied at each & every price. Causes of shifts in supply:

- Improvements in technology (increase efficiency & reduce costs).

- Weather, climate and disease (especially agricultural products).

- Taxes and subsidies can make the costs of production more/less expensive and therefor increase or decrease supply.

- Natural disasters & wars can severly disrupt supply.

- Resources: discoveries of new resources or depleting reserves of resources can affect the supply of products.

Elasticity of Supply

In economics price elasticity of supply means the

degrees of responsiveness of quantity supplied of

commodity X to the change in price of X itself.When price of X changes, supply for it may change

either proportionately; more or less than

proportionately; or may not change at all. These

changes can be expressed in %s as under

Es = % change in Quantity supplied of X

_______________________________________

% change in Price of X

Thus price elasticity of supply is the ratio of

percentage change in quantity supplied of X to

percentage change in price of X.

Therefore,

%ΔQsx

Es = ________

%ΔPx

Or mathematically it can also be expressed as

P ΔS

Es= __ x ___

S ΔP

Five Types of Elasticities of Supply - Es :

1. Unit Elastic Supply

Supply is said to be unit elastic when elasticity

of supply is = 1. Then any change in price brings

about exactly proportionate change in quantity

supplied.

2. Relatively Inelastic Supply

Supply is said to be Relatively Inelastic when

elasticity of supply is < 1. Then any change in

price of commodity X, brings about less than

proportionate change in quantity of X supplied.

3. Relatively Elastic Supply

Demand is said to be Relatively Elastic when

elasticity of supply is > 1. Then any change in

price of commodity X, brings about more than

proportionate change in quantity of X supplied.

4. Perfectly Inelastic Supply

Supply is said to be Perfectly Inelastic when

elasticity of supply is = 0. Then any change in

price of commodity of X brings about no change in

quantity supplied.

5. Perfectly Elastic Supply

Supply is said to be Perfectly Inelastic when

elasticity of supply is = α. Then any negligible

change in price of commodity X. brings about

infinite change in quantity of X supplied.

All five types of elasticities of supply can be

shown by different slopes of supply curve.

► Unitary elasticity of supply

Change in price from OP1 to OP2 brings

less than proportionate change in quantity

supplied from OQ to OQ1.

► Relatively Inelastic Supply

Change in price from OP to OP1 brings less than proportionate change in quantity supplied from OQ to OQ1.

► Relatively Elastic Supply

Change in price

brings more than proportionate

change in quantity supplied.

► Perfectly Inelastic Supply

Change in price brings no change in

quantity supplied.

► Perfectly Elastic Supply

Negligible change in price

brings infinite change in quantity

supplied.

Time Element and Supply

Economist Marshall assigned considerable importance

to time in the determination of supply. He stated

that demand reacts to a price change immediately.

But supply takes some time to adjust to price and

demand changes. Supply today is a function of

price prevailing in the immediate past.

Depending upon the period of time, supply can

adjust itself either partly or fully or not at all

to the change in demand and price; and will in turn

influence price. For supply to adjust to the

changes factors of production and process have to

be readjusted or investments increased. This

requires certain time.

Marshall has classified time into four categories.

♠ Very short period:

In this short time supply cannot adjust to change

in demand.

♠ Short period:

In this short time available, supply can adjust

partly to the change in demand by adding

(only) variable factors of production towards

supply.

♠ Long period:

In the long period, supply can adjust more fully to

the change, as adequate time is available to add

both variable and fixed factors of production

and/or increase capacity.

♠ Very long Period:

Nothing is certain about demand and supply in the

long period. Keynes said, “in the long period we

are dead”

Time element plays an important role in the theory

of price through its influence on supply.

No comments:

Post a Comment